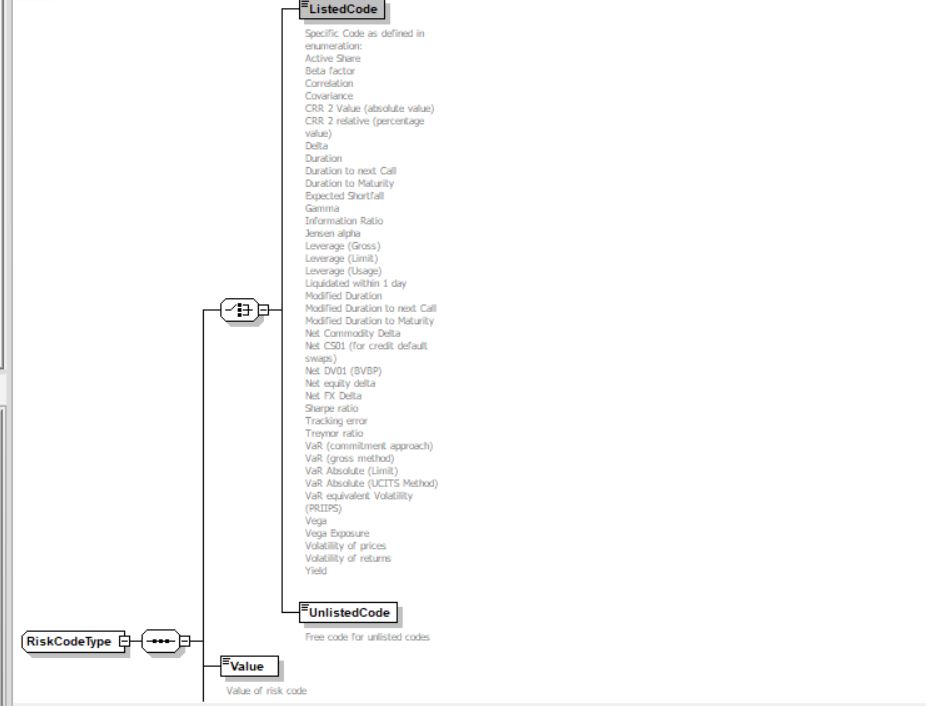

The FundsXML initiative has published a new version of the FundsXML Schema. In the new version 4.1.10 the enumeration list in RiskCodeType is extended by the entries “CRR II Absolute” and “CRR II Percentage” (//element(*,RiskCodeType)/ListedCode). This allows users to specify the Credit Risk Ratio according to the Capital Requirements Regulation (CRR II), both on the fund level as well as on the portfolio level.

Additionally, the indicator “VaR equivalent Volatility” according to PRIIPs was added.

Beyond minor bug fixes, the new version 4.1.10 also includes an Interest-rate swap as a new Swap type (/element(*,SwapType)/Type).